The 2020 edition of the United Nations Economic Commission for Europe (UNECE) and the Food and Agriculture Organization of the United Nations (FAO) Forest Products Annual Market Review provides a statistical review of market developments in the UNECE region in 2019 and the first half of 2020 (including initial impacts from the COVID-19 pandemic) and the policies driving those developments.

The global UNECE forest region is divided into three subregions: Europe; Eastern Europe, Caucasus and Central Asia (EECCA), and North America. It encompasses about 1.7 billion hectares (ha) (4.2 billion acres) of forest, which is more than 40% of the world’s total forest area.

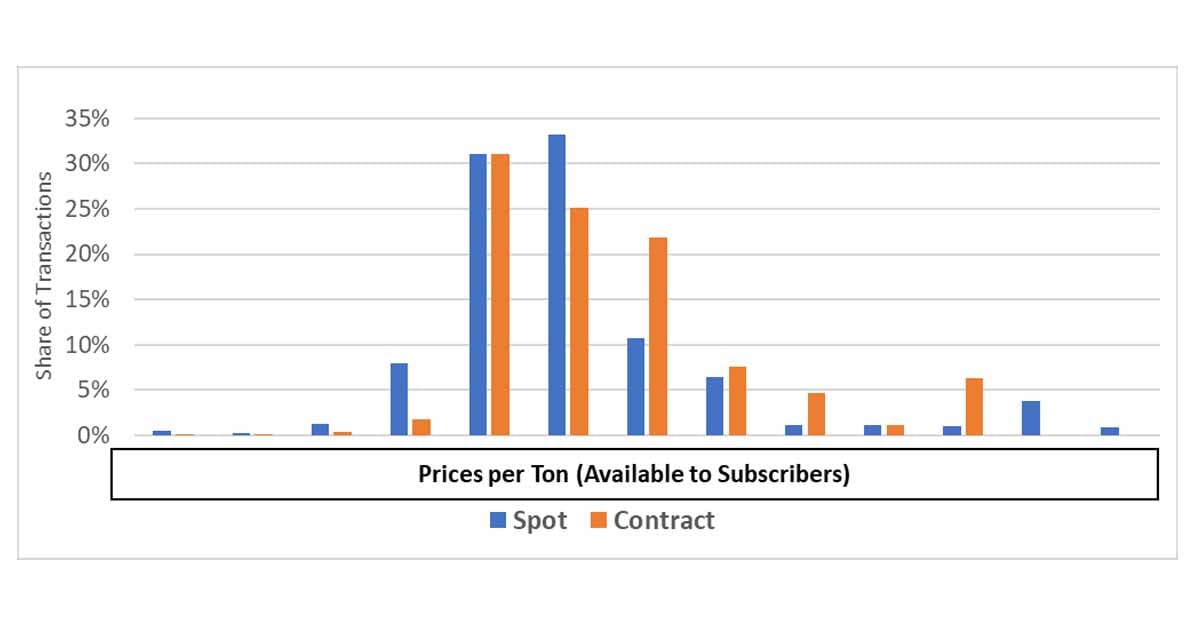

The following are direct excerpts and key insights by wood product category from the latest Review using data from 2019 and 2020:

Economic Activity

- Economic activity decelerated markedly in the UNECE region in 2019. The slowdown, which was generalized and affected all subregions, occurred against a background of increasing trade tensions, slower global growth and increasing uncertainty. This adverse external context depressed manufacturing and dampened capital spending, particularly affecting those economies most exposed to global trade.

- The economic outlook is highly uncertain in light of the COVID-19 pandemic, with no clarity on its duration, the spread of the virus or the need for further restrictive measures. Nevertheless, there has been a bounce in economic activity (from very depressed levels) with the easing of mobility restrictions, supported by significant policy stimulus.

Roundwood Consumption

- The total consumption of roundwood – comprising logs for industrial uses and fuel – in the UNECE region was estimated at 1.4 billion cubic meters (m³) in 2019, the first decrease after six consecutive years of increase. The apparent consumption of logs for industrial purposes was down by 3.2%, to 1.16 billion m³, although this was still 7.5% higher than in 2015. Of the total volume of roundwood harvested in the UNECE region in 2019, about 18% (260 million m³) was used for fuel, a decrease of 3.7 million m³ (-1.4%) compared with 2018.

Pulp & Paper

- The global pulp, paper and paperboard industry experienced general weakness in 2019 compared with 2018 (when pulp prices reached record levels and paperboard demand was strong). The production of graphic paper declined due to closures and reduced consumption, the result of increased electronic communication. In contrast, growth continued in the consumption of sanitary and household papers, certain paperboard products and specialty papers, and pulps, including fluff and dissolving.

- Prices for printing and writing papers and newsprint fell in EECCA in 2019 due to weaker demand, but prices for paperboard and tissue were relatively stable. Prices for market pulp fell considerably in 2019 after a rapid rise in 2018.

- Prices for printing and writing papers and newsprint fell in EECCA in 2019 due to weaker demand, but prices for paperboard and tissue were relatively stable. Prices for market pulp fell considerably in 2019 after a rapid rise in 2018.

- The production of graphic papers declined throughout the UNECE region in 2019 – by 7.1% in Europe, 0.2% in EECCA and 11.2% in North America. Apparent consumption also fell in the three subregions – by 7.1% in Europe, 10.4% in EECCA and 10.7% in North America.

- The apparent consumption of packaging material in 2019 fell in Europe (by 2.8%, the first decline since 2011) and North America (by 1.7%, the first drop since 2013); on the other hand, it increased by 2.4% in EECCA.

- Overview of pulp production in each region

- Europe: Total pulp production in Europe fell by 0.19% in 2019 due to weaker graphic-paper demand. The production of paper and paperboard was down by 3.2% in 2019, at 95.6 million tons. Graphic paper production fell by 7.1% and resulted in machine closures.

- Eastern Europe, Caucasus and Central Asia: Chemical woodpulp production fell by 2.6% in EECCA in 2019, which was the result of higher maintenance outages in the Russian industry. Paper and paperboard production and consumption was flat in the subregion in 2019, and while the pulp industry grew in parts of the EECCA with new capacity (Belarus), paper and paperboard production fell by 0.6% to 10.9 million tons.

- North America: Production of woodpulp dropped by 1.6% in 2019, and chemical pulp production and apparent consumption fell by 1% to 54.3 million tons and 2.5% to 45.8 million tons. Along with this, North America’s production of paper and paperboard dropped by 4.2% in 2019 to 77.6 million tons.

Initial data supplied by UNECE member States indicate the production of paper and paperboard will decline in the UNECE region by 2.6% in 2020 and 2.0% in 2021. Subregionally, the forecast is for paper and paperboard production to decline in Europe by 4.8% in 2020 and remain steady (+0.1%) in 2021; increase in the EECCA by 1.0% in 2020 and by 1.6% in 2021; and North America to shrink by 1.1% in 2020 and 4.3% in 2021.

For a granular view of what’s happening in the pulp & paper industry - down to the mill level – talk to us about the benefits of using the FisherSolve business intelligence platform. FisherSolve contains highly detailed and complete information on every pulp and paper mill in the world. It describes the assets, production, operations, environmental flows, costs-of-production, long-term viability, carbon footprint and more for all pulp and paper mills producing 50+ TPD. Because this is the only industry database with integration and true data transparency, you can drill down to the details that differentiate each mill and roll the details up for the strategic analyses that matter most to you.