This abridged article, which originally appeared in Tissue World Magazine, presents a static picture summary of Canada’s tissue industry.

Canada enjoys the world’s longest demilitarized border with its only land neighbor, the United States. It is a vast country, but the population tends to concentrate along the southern border with the United States. As a result, Canada’s consumers tend to be more like Americans, and this extends to tissue paper consumption rates and habits.

United States tissue companies Scott Paper and Procter & Gamble once had a significant presence in the country. Kimberly-Clark is now the only USA-based company operating a tissue mill in the country and Canadian tissue makers are increasingly buying and building assets south of the border including Kruger, Irving, and Cascades.

The recently refreshed trade agreement between Canada, the United States and Mexico continues to support strong trade ties.

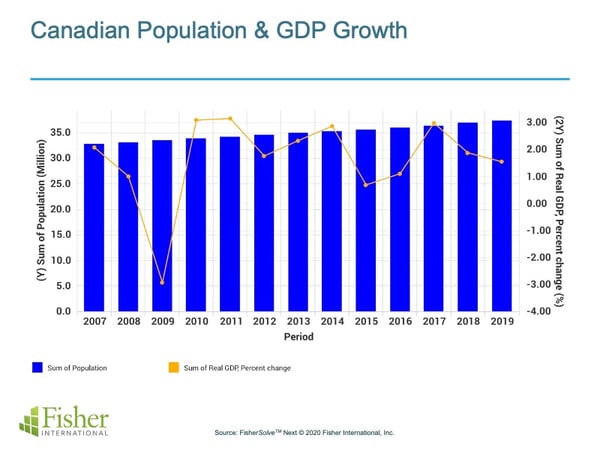

Canada’s 2019 population is shown in Figure 1at just under 36 million, growing at about 0.72% per annum, which is only about 10% of the population of the United States. Figure 1 also shows the country’s real GDP growth rate dropping with the global recession of 2007 and then recovering to about 3% growth and settling out to about 2% in 2019.

FIGURE 1

FIGURE 1

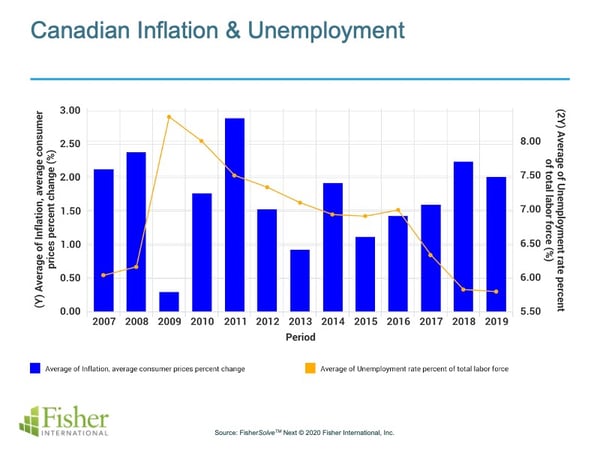

Figure 2 shows unemployment and inflation over the same period. Unemployment spiked from about 6% in 2007 to almost 8.5% in 2009. Unemployment has steadily decreased over the next ten years of economic recovery. Inflation is also shown in Figure 2, tracking at just under 2%. Canada’s economy is more focused on natural resources than the United States resulting in occasional divergences.

FIGURE 2

FIGURE 2

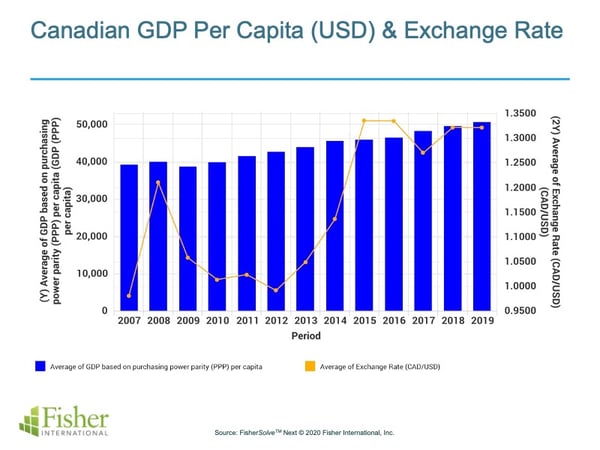

Canada’s close relationship with the United States requires some comparison to evaluate the economics of consumer demand. Figure 3 illustrates the adjusted Canadian GDP purchasing power per capita over the recovery period as blue bars. The line graph shows the relative Canadian dollar currency strength versus the US dollar. The wide swings shown are frequent and alternatively enjoyed by consumers crossing the border for shopping.

FIGURE 3

FIGURE 3

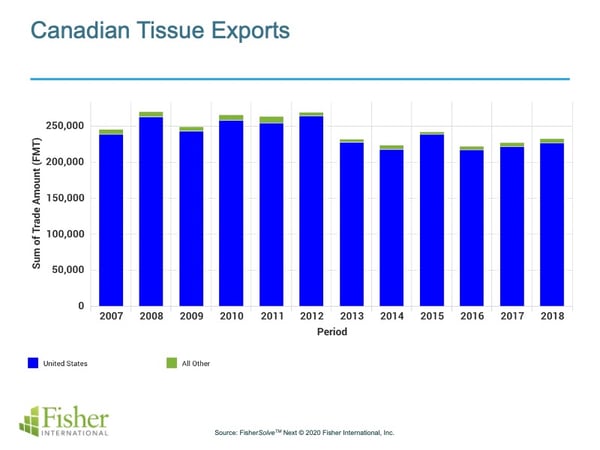

Tissue Trade volume analysis is required to evaluate the region’s consumption and production. FisherSolve™ Next provides quick access to UN trade data to help visualize the trend. Figure 4 shows the trend of tissue exports from Canada to the top importers. The United States is the top destination for Canadian tissue exports with “all other” represented by a small slice. The total volume of tissue exports has decreased somewhat over this period, while domestic demand has grown.

FIGURE 4

FIGURE 4

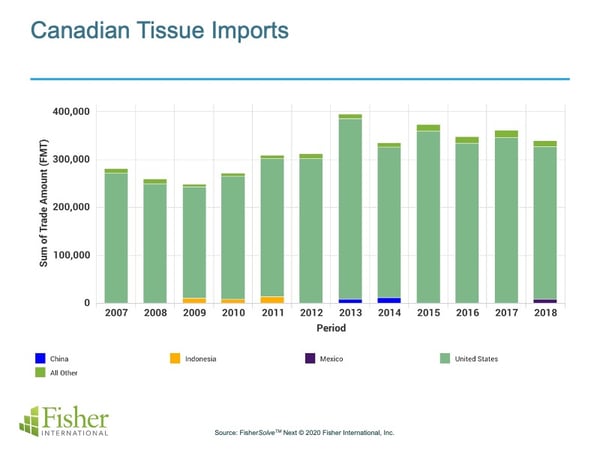

Figure 5 shows the trend of Canada’s tissue imports for the same period, which have tended to be steady to slightly increased over the past five years. Tissue imports tend to run about 75,000 finished metric tons ahead of the tissue exports shown in Figure 4. The top tissue supplier for Canada is the United States, with small contributions from China, Indonesia, and Mexico. These trade partners and the United Kingdom (following Brexit) and Brazil, with low-cost integrated-fiber tissue, provide a basis for comparing Canada tissue machine quality versus relevant competition.

FIGURE 5

FIGURE 5

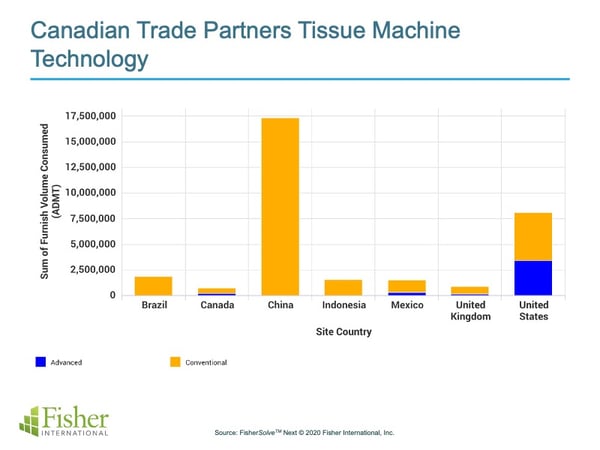

Canada’s average tissue machine quality (old and small) is relatively low compared to its trade partners. Machines in the United States also tend to be older but are noticeably wider, however, Mexico and Indonesia have newer and wider machines than Canada. China’s machines are very new on average but tend to be very narrow.

Figure 6 shows the deployment of tissue advanced technology across the trade partner comparison group. Only the United States, Mexico, and the UK have the advanced tissue production capacity that Canadian consumers are expecting.

FIGURE 6

FIGURE 6

Canada has largely recovered from the global recession that began in 2007; personal income is growing and population growth is slow but positive, in part due to an increase in immigration. Canada’s tissue producers are stable and expanding on both sides of the border with the United States. It is reasonable to expect that tissue consumption will continue to grow per capita in addition to the small population growth.

While Canada’s tissue machines tend to be narrower and older compared to other global producers, the added input capacity has resulted in an improvement trend. Capacity growth is at a deliberate pace as several of the producers are also investing south of the border. Advanced tissue technology is a larger than average share of production, second only to the United States. The lower carbon content of Canada’s electric power is a major advantage, and this is expected to become a differentiator.

Will Canada’s production continue to grow or will imports from the United States replace a larger portion of market demand? The renewed trade agreement and Canadian controlled investment south of the border warrant watching.

Pulp and paper producers use Fisher’s business intelligence resources for both market and competitive analysis. From strategic decisions about products and assets to tactical decisions like where to spend sales time, we support the entire decision chain with the FisherSolve™ platform.