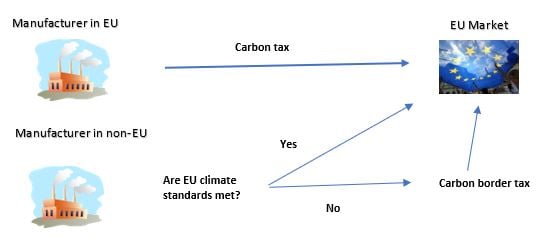

In July 2021, the European Commission announced plans for the EU Carbon Border Adjustment Mechanism (CBAM), which, simply put, is a carbon border tax. The concept of a carbon tax is nothing new, as we’ve seen it implemented in California through its ‘cap and trade’ system. However, this will be the first time such a tax will apply to imports.

How Will the CBAM Work in Practice?

The CBAM system will work as follows: EU importers of certain products will buy carbon credits equivalent to the carbon price that would have been paid if the goods had been produced under the EU's carbon pricing rules. Conversely, a non-EU producer who can demonstrate that it has already paid a price for the carbon used in the production of the imported goods in a third country will be able to deduct the full corresponding cost to the EU importer.

Which Sectors Will be Impacted?

The CBAM will initially apply to the imports of the following goods:

- Cement

- Iron and steel

- Aluminum

- Fertilizers

- Electricity

There will be a transitional phase from January 1, 2023 to December 31, 2025 in which importers must calculate and report emissions, but they will not yet have to pay a carbon border tax. The implementation phase will start on January 1, 2026, meaning that importers will have to purchase import permits and begin paying the border tax.

However, one of the main questions raised by this new policy is how will industry participants and importers quantify the carbon emissions accurately and systematically?

Under the Commission’s proposal, importers will have to report the emissions embedded in their goods without paying any financial adjustment in the transition phase. In other words, importers will calculate and report carbon emissions themselves, without supervision or monitoring. Can this be accurate and trustworthy? The mechanism developed to calculate carbon emissions must cover the entire supply chain, including sourcing, production, delivery, etc. If sourcing or production takes place in a non-EU country, how can it be aligned with EU standards? If importers fail to ensure that emissions are properly declared, will they be liable for non-compliance? Or should this data be independently verified?

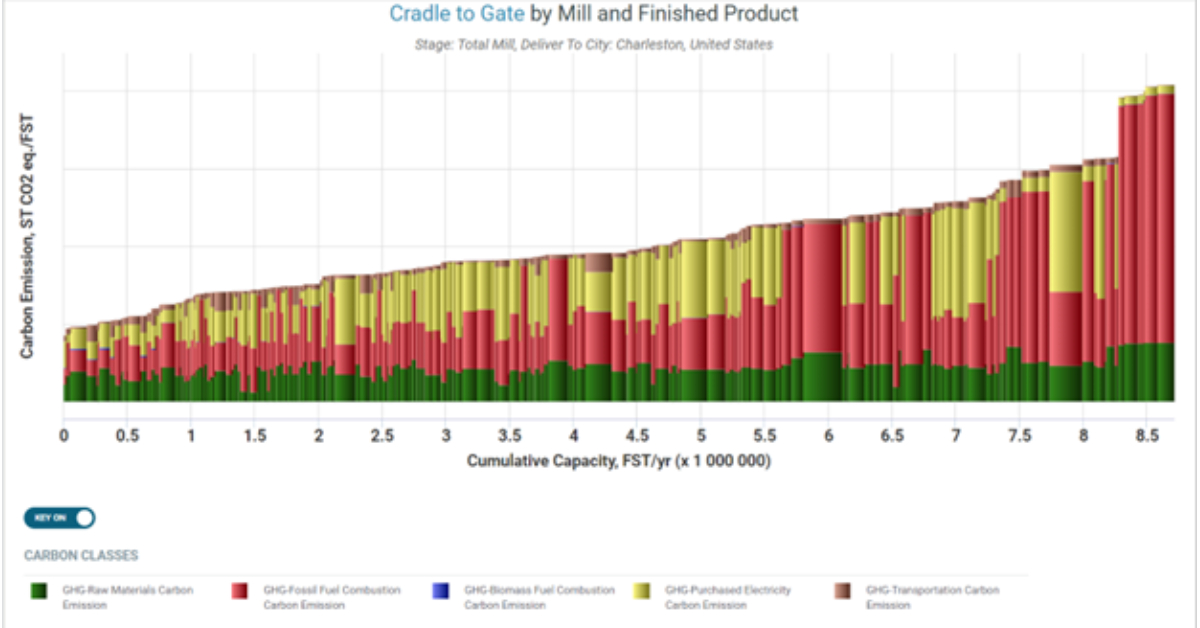

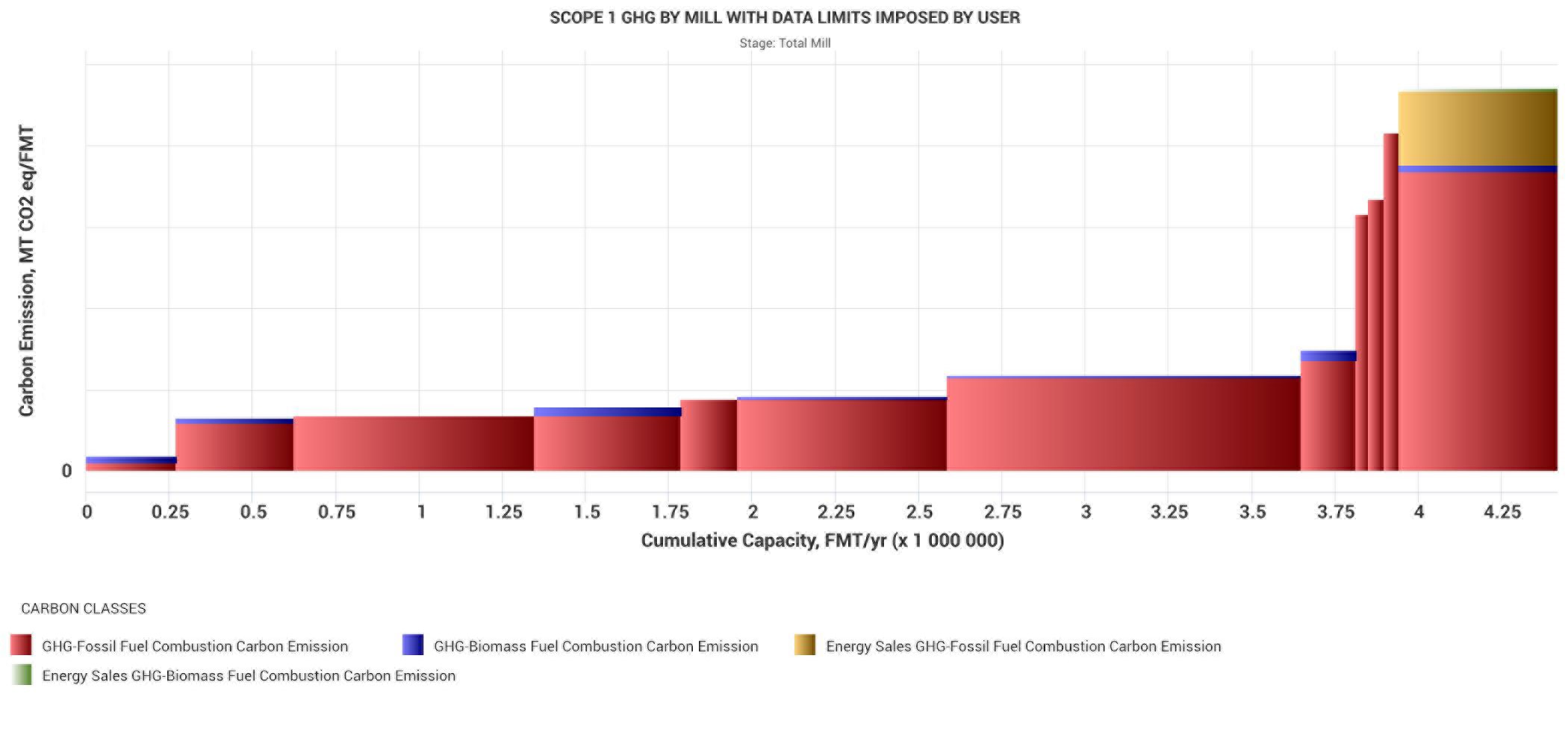

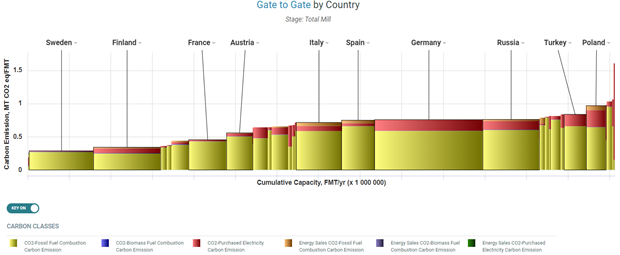

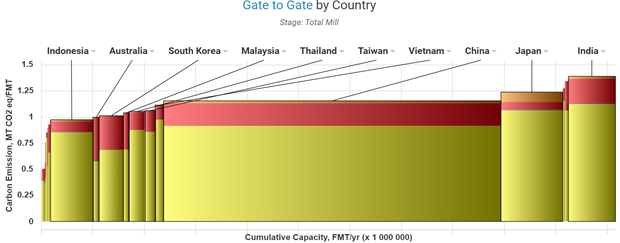

The graphs below illustrate the carbon emissions capacities of the paper industry in the EU and the Asia-Pacific region. These figures demonstrate the significant difference in carbon emission volumes between the two regions.

Carbon Emissions from Top 10 Countries with the Largest Capacity in EU 2Q2021

Source: FisherSolve™ Next

Carbon Emissions from Top 10 Countries with the Largest Capacity in Asia Pacific Region 2Q2021

Source: FisherSolve™ Next

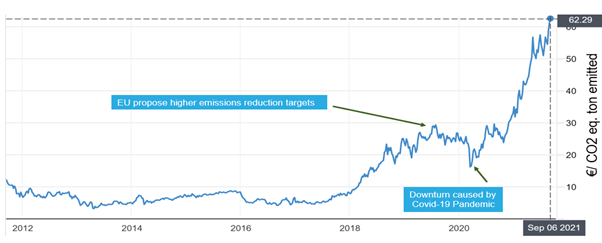

Another important question to consider is: How can industry participants quantify the impact the carbon border tax will have on emissions after implementation? The carbon border tax is designed to ensure that domestic companies remain competitive and are not tempted to relocate. The results of the UN Conference on Trade and Development (UNCTAD), which analyzed various scenarios, show that a price of $44 per tonne of CO2 would reduce carbon leakage by half. Below we can see the price development for carbon dioxide in the EU as a reference.

EU Emission Trading Scheme (ETS) Reached an All-Time High in 2Q2021

Source: Tradingeconomics.com

Even though the CBAM system won’t be implemented for another few years, the impact it could have on the P&P industry will be significant. It is therefore critical that manufacturers and suppliers keep a close eye on how the transitional phase plays out in the coming months and years, and what steps innovative players will take to prepare for the inevitable change.