China’s Belt and Road Initiative is a global infrastructure development strategy adopted by the Chinese government that aims to invest in nearly 70 countries and international organizations. The initiative is poised to boost international trade, and it has the potential to accelerate economic growth across Asia, Central and Eastern Europe.

As part of the initiative, the China-Russia and China-Europe railways are already improving delivery capacities in the region. Per a recent article in Xinhua, “Foreign trade volume by railway through Manzhouli, the largest land port on the China-Russia border, exceeded 10 million tonnes in the first half of this year, up 6.4 percent year on year, according to official figures.”

Major commodities moved across the border included coal, wood raw materials and construction machinery. China’s pulp and paper industry is also benefitting from the expansion in trade.

“A total of 1,505 China-Europe freight trains passed through the port in the first half, an increase of 19 percent compared with the same period last year, carrying 134,700 TEUs of goods in total,” Xinhua said.

The rail routes have also become an important transport channel for stabilizing global trade and recovery amid the COVID-19 pandemic, and authorities in the port of Manzhouli have increased efficiencies and reduced logistics and transportation costs. Manzhouli has become an important destination for shipments of pulp to China, which is oftentimes routed to manufacturers in Hebei Province.

According to statistics from Manzhouli customs, in the first half of 2020, 236,000 tons of pulp were imported through the port, an increase of 99.9% over the same period last year, with a value of 830 million yuan—an increase of 57.5%.

Pulp & Paper Insights

Three rail routes have been laid out along the western, middle, and eastern territories: The western passage leaves China through the Alashankou (Horgos) in the central and western parts the country; the middle passage through Erlianhaote from North China, and the eastern passage via Manzhouli from the coastal areas in the eastern parts of China.

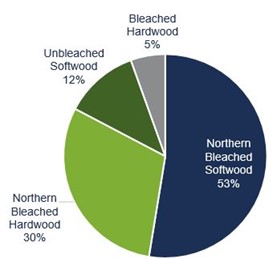

As a major global consumer of wood pulp, accounting for about 35% of total demand, China primarily relies on imports to meet its demand. In 2019, China imported roughly 23 million tons of market pulp, including about 10 million tons of softwood pulp. Canada (27%), Chile (16%), Finland (15%), the United States (14%) and Russia (11%) were the top five exporters supplying this softwood pulp.

There are vast coniferous forest resources in Russia, and the manufacturing cost is relatively low. Looking at the cash production cost of NBSKP via the cash production cost module in FisherSolve Next, we can see that Russia has the lowest average cash production cost in the world (260-270 USD / BDT), which is about 25-30% lower than the average cash production cost of Canada. According to Fisher data, the current production capacity of market wood pulp in Russia and Belarus is roughly 3 million tons, of which coniferous pulp accounts for about 65%.

Over the next five years, about 5 million tons of market pulp capacity will enter the supply chain, of which about 3 million tons will be coniferous pulp, which will greatly increase global demand.

Fisher believes that after the total ban on imported RCP that will take effect in 2021—along with the impact of growing anti-plastics sentiment and the transition to more paper packaging—China’s demand for market pulp will increase in the future. Due to its unique position in an expanding market (low fiber costs, location, and position in the Belt and Road Initiative), Russia is poised to become one of the most important market pulp suppliers for China’s robust pulp and paper industry.